December 2023 - Headwinds that have faced listed real estate for the past two years.

by Stephen Bennie 2023-12-20

2023 has been a pivotal year for the New Zealand listed retirement sector, but not in a share price sense. The share price damage was largely done in 2022as the sector experienced a broad de-rating as the short-term effects of falling house prices impacted investor sentiment. The key pivot this year has been a changing strategic direction for the retirement operators.

At Castle Point we have long been under-weight in the sector versus a benchmark such as the ASX/NZX 50 index, a call which did not cover us in glory from 2013 to 2021 as the retirement sector performed strongly. We certainly understood the bull case for being positive on the sector. Yes, there are strong demographics supporting the sector as our society fills up with over 75-year-olds keen to live in a plush retirement village. Yes, it has a great self-funding dynamic that customer upfront cash payments can be used to develop more units to sell to more customers that allows even more growth. Yes, and of course residential property prices in New Zealand only go up.

The concern that we had though, was that due to the ever-increasing build rate the operators overall portfolio of retirement villages was not of a vintage that generated positive free cash flow. At times, as the 2010s progressed it felt like retirement operators were increasing their build rate to support further share price gains. This in turn suppressed the average age of their villages lower as more new supply was added to the portfolio of villages. Ironically this supported our reticence regarding the sector while driving their share prices higher. Effectively we were right but wrong regarding share price direction, at least until 2021.

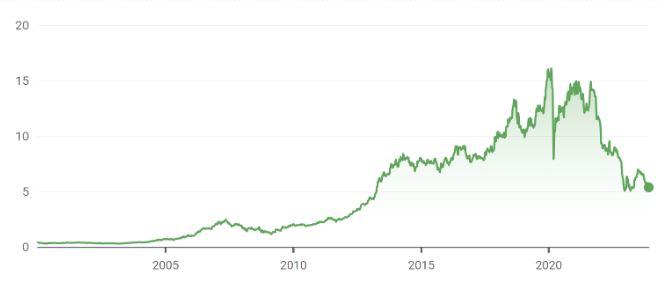

Ryman Healthcare flew too close to the sun in 2021

Source NZX.

Jump forward to 2023 and things have changed. The sector appears to have been forced to take a leaf out of John Key’s play book. I’m sure readers will recall that Key was an adept political operator and one of his canny abilities was to realise when a policy direction was proving unpopular. Invariably he would respond to that by reversing directions, but he knew that dithering over such a change was not a great look. No; such a change had to be done quickly and with conviction. And of course, ditching an unpopular policy improves your popularity. While not as quick or deft as Key, the retirement sector is turning from a focus on a rapid as possible build rate, to a focus on cash generation to reduce debt.

The unpopular policy direction that the retirement sector is having to reconsider is that investors are no longer happy to see debt mount up. There are two main reasons for this. Firstly, debt is now expensive because interest rates have risen and secondly because lenders are more risk averse than they were. The US regional banking crisis was really the cherry on top of the cost of debt rising to levels not seen in over two decades. Ideally investors would now prefer zero debt, part of the popularity of US Mega Cap growth stocks. If you can’t quite deliver zero debt, investors are looking for moderate debt levels and if you can’t quite manage that, then you better be reducing it and the quicker the better.

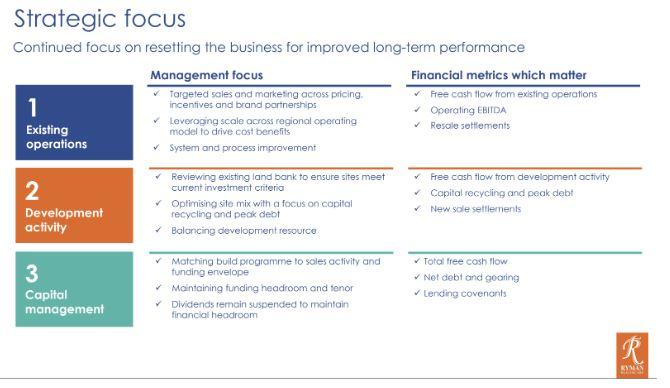

This pivot can be well illustrated by looking at the recent Ryman Healthcare result. Back in February, when they raised capital to pay back their US Private debt holders, they committed to becoming free cash flow positive by their 2025 Financial Year end5. This effectively meant that their net debt would rise in the intervening period which is not exactly hitting the mark of quickly reducing debt. So it was not too surprising to see that in last months result they demonstrated an increased focus on generating free cash flow. As you can see below, for every strategic goal the most important financial metric is now free cash flow.

Ryman now focused on generating free cash flow

Source: Ryman Healthcare

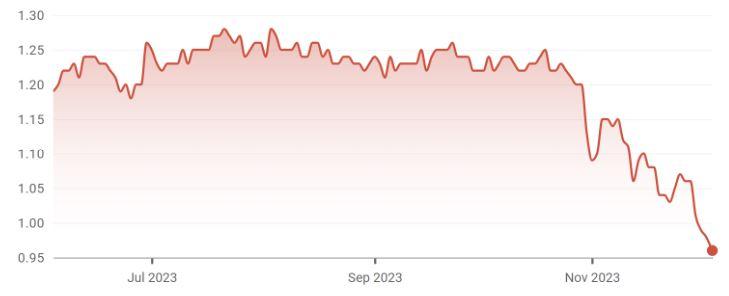

That said, some what bizarrely, not every retirement sector operator got the memo about reducing debt. On 31st October Arvida announced that they had restructured its debt facilities and that its total drawn debt was now $755 million6. Interestingly the Arvida CEO namechecked ANZ, BNZ and ASB as its banking syndicate. We can only speculate as to whether Westpac were feeling unhappy or relieved not to be lenders. However, we can be pretty sure that Arvida shareholders were unhappy. At the time of writing this article, the Arvida share price has dropped by more than 20%since that drawn debt update at the end of October. I have a rule of thumb that when the debt owed by a company, I’m invested in, exceeds the size of its market capitalisation, I’m often left wishing I didn’t own it. Perhaps I’m not the only investor that has that rule.

Can you guess the day Arvida announced a 25% increase in debt?

Source: NZX

So, Arvida aside, the listed New Zealand retirement sector has moved from growing and increasing debt to seeking cash generation. The conundrum facing investors, is what is the value of a retirement village operator that is no longer a growth vehicle? Frankly, I do not have the answer to that question. I do know that you tend to face an investor migration as the shareholder base of a company changes. Growth investors are natural sellers while value investors become sporadic buyers in such a situation. A rotation of a shareholder base like that does not happen over weeks or months, it tends to take longer. However, the process will be all the smoother the quicker the listed retirement operators can become free cash flow positive. The go-go days appeared to have passed and it’s now time for the retirement sector to show investors the money.

Share article:

Other Insights

Stay updated with Castle Point Funds.

Investments

Resources

Company

Castle Point Funds

Perpetual Guardian Tower

Level 23, 191 Queen Street

Auckland 1010

PO Box 105889

Auckland 1143, New Zealand

E info@castlepointfunds.com

PG Funds Limited is the issuer and manager of the Castle Point Funds Scheme.

2025 Castle Point Funds, Inc. All rights reserved.

Privacy Policy