October 2023 - Gauging the increasing number of write downs

by Stephen Bennie 2023-10-17

I recently wrote an article for Margin Call on the deeply engrossing topic of “non-cash” one off write-downs or losses. At the heart of that article was that while companies prefer investors to essentially ignore such write downs because they deem them “non-cash”, the reality is that the “non-cash” description is somewhat misleading as they are “non-cash” in terms of the current financial year. Typically though actual dollars have gone up in smoke, just in an earlier financial year. I gave the example in that article of overpaying for an acquisition and in later years writing the value of that acquisition down. Real cash lost when the acquisition was acquired; “non-cash” lost in the following years when the acquisition is written down.

In that article I focused on the annual result of SkyCity which included a classic example of a “non-cash” write down of the book value of its Adelaide Casino. However, as the August reporting season progressed there seemed to be an unusually large number of varying “non-cash” write downs or abnormal items by those companies releasing their annual or interim results. So, with the aid of Forsyth Barr, I decided to tally up the score card and have a closer look to see if any trends were emerging regarding “one-off” abnormal items. The study compared reported earnings for the past eight years for 39 companies that report in August with their normalised earnings, the difference between the two being “one-off” abnormal items.

First the positive “one-offs” from this reporting season. Vector and Spark both posted abnormally large reported profits due to selling some assets which are reported as abnormal items. This year Vector sold a 50% stake in its metering business to QIC Private Capital for the tidy sum of $1.75 billion.

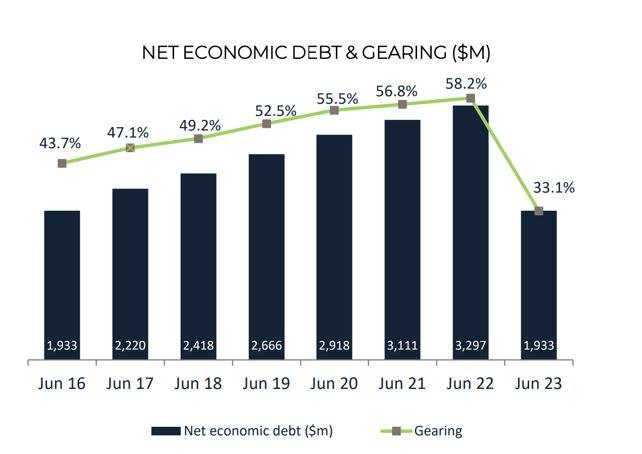

Shareholders received a special dividend of 5.5c but the bulk of the proceeds were used to pay down debt which had been trending in an upwards direction in recent years.

Vector Group debt profile in recent years

Source NZX

Meanwhile Spark sold 70% of its TowerCo infrastructure division to the Ontario Teachers Pension Plan for $911 million, $350 million is being used for a share buy back and the balance to reduce debt. Both sell downs of assets resulted in large gains for Spark and Vector in the financial year just passed.

However, of the 39 company results that we looked at 23 of them contained a negative “one-off” abnormals. For this group of companies that is the highest number of write-downs over the past 8 years of audited financial results. The average number of write-downs over this period is 13. So the hunch of a particularly high number in this reporting season was a correct one. However, I would also note that with a solid third of the sample companies now posting an abnormal item, that they are an endemic aspect of corporate results. As such I would hesitate to readily ignore them as inconsequential “one-offs” when they appear to happen so frequently. The table below provides a top-level review of the study.

Negative abnormals of companies that report in August.

Source: Forsyth Barr & NZX

As well as frequency of abnormal items, another important feature is the size of the write-down. My hunch was that the quantum of write-down in this reporting season was also high. As the above table shows that was indeed the case with a total of $1.6 billion of negative abnormals. This is only surpassed by the $1.8 billion that vanished in Financial Year 2019. Out of interest, over 80% of that total was down to just two companies, Fonterra and Sky TV who wrote down the book value of their businesses by $801 million and $705 million respectively. For Fonterra that was principally a reassessment of the value their operations in China and Brazil, while for Sky TV it was essentially an acknowledgment of the impact of Netflix and other streaming services coming to New Zealand. This years negative abnormal are much more broadly spread with Precinct Properties, Vital Healthcare, Meridian Energy, Fletcher Building, Mercury, SkyCity and Auckland Airport, all reporting negative abnormals ranging from between $260 million and $100 million.

So, in broad terms we are seeing an increase in the number and level of negative abnormals over the past eight years. What is driving that and what does it mean for investors. My overriding observation is that it is getting harder to ignore abnormals as they become more prevalent in annual results, which I believe supports what was the main thrust of my previous article on this topic.

However, this study has raised some additional observations. Some business models are more susceptible to write-downs as well as write ups, a prime example of this being listed REITS as the value of their properties gets pushed around by interest rates. For most of the last 8 years they benefited from falling interest rates but this year the opposite was the case. For example, the two largest negative abnormals were by Precinct Properties ($260 million) and Vital Healthcare ($222 million) while Auckland Airport chipped in $105 million due to its property division. The current downward trajectory of listed REITS share prices suggests that investors see more negative write-downs still to come from that part of the market.

Another observation of this August reporting sample of companies is that it is very slim pickings for investors that want to own companies whose reported earnings consistently match their normalised earnings. Only three of the 37 companies reported no abnormal items over the past 8 years: Chorus, Hallenstein, Glasson and Skellerup. This again underlines the reality that investors have to deal with abnormals but shouldn’t necessarily ignore them.

Share article:

Other Insights

Stay updated with Castle Point Funds.

Investments

Resources

Company

Castle Point Funds

Generator Britomart Place

Level 10, 11 Britomart Place

Britomart, Auckland 1010

PO Box 105889

Auckland 1143, New Zealand

E info@castlepointfunds.com

2024 Castle Point Funds, Inc. All rights reserved.

Privacy Policy