July 2023 - Emissions Trading Scheme – not meeting our long-term climate goals

by Stephen Bennie 2023-07-06

There has been quite a bit written on the Emissions Trading Scheme (ETS) in recent weeks and months as a lot of upheaval has occurred. For those less familiar with the ETS, it was launched nearly 20 years ago and is currently the main tool NZ has to incentivise emitters to reduce or offset their carbon emissions by the market setting a price for each ton of CO2 emitted.

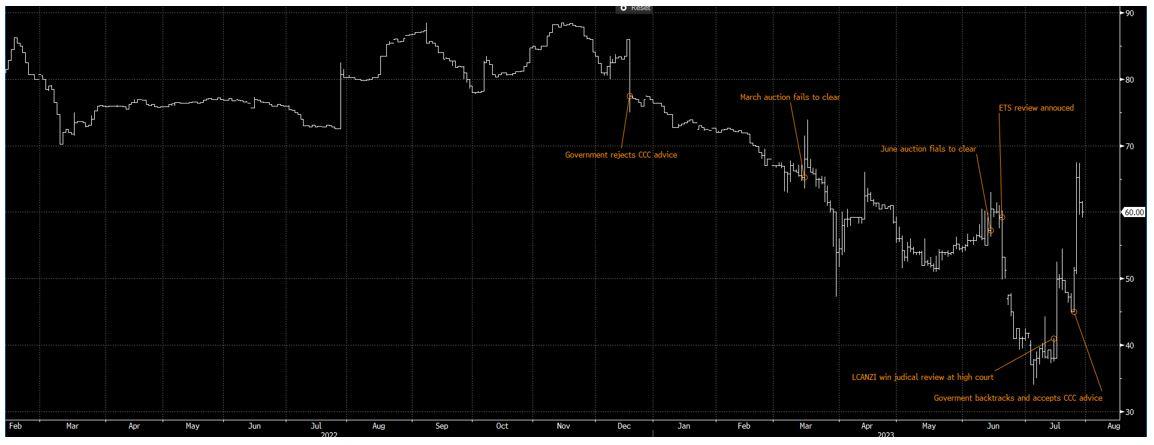

For those that have been following the ETS market you see below that the price for one NEW Zealand Emission Unit (NZU) peaked at close to $90 at the end of 2022. Since then, things have unfolded quite dramatically. Firstly, the government decided, in December 2022, to reject the Climate Change Commission (CCC) advice on ETS settings for the next 5 years (2023 – 2027). The CCC annually provides advice on the price settings for the upcoming 5 year period. The CCC advice recommended settings that would reduce the amount of units that could be issued under auction and put higher price triggers and floors – all designed to strengthen the price signals and increase gross emission reduction. The key reason the government gave when announcing they were rejecting these recommendations was that they could contribute to inflationary pressures. This was the first leg in reduced confidence in the ETS market. Notably in April 2023 the CCC released the next set of advice on the next 5 year period (2024 – 2028) and in essence doubled down on their earlier advice.

Source: Bloomberg, Castle Point

Then in June 2023 the government announced a review of the ETS scheme. This review was driven by CCC advice that the current modelling of the ETS highlighted that it was likely to promote significant planting of exotic forests (i.e. Pinus Radiata). These new forests would generate a lot of NZUs which would start to flood the market from 2030’s and potentially lead to a depressed NZU price, which would send the price signal to firms with CO2 emissions that it could be cheaper just to buy NZUs to offset their carbon emissions rather than invest into reducing the gross emissions. This review is a valuable discussion and highlights that regulatory schemes often have unintended consequences and changes can be needed to ensure the scheme continues to deliver the desired outcomes.

It is important to note that this scenario of a NZU price that falls dramatically in 2030’s due to a glut of units from forestry does not help anyone – it is disappointing for forest owners that have planted based on expected higher prices, it does not encourage firms to reduce gross emissions, it reduces government income from the auctions, and overall would likely lead to NZ as a whole struggling to meet the longer term Nationally Determined Contribution (NDC) we have signed up to through the Paris agreement.

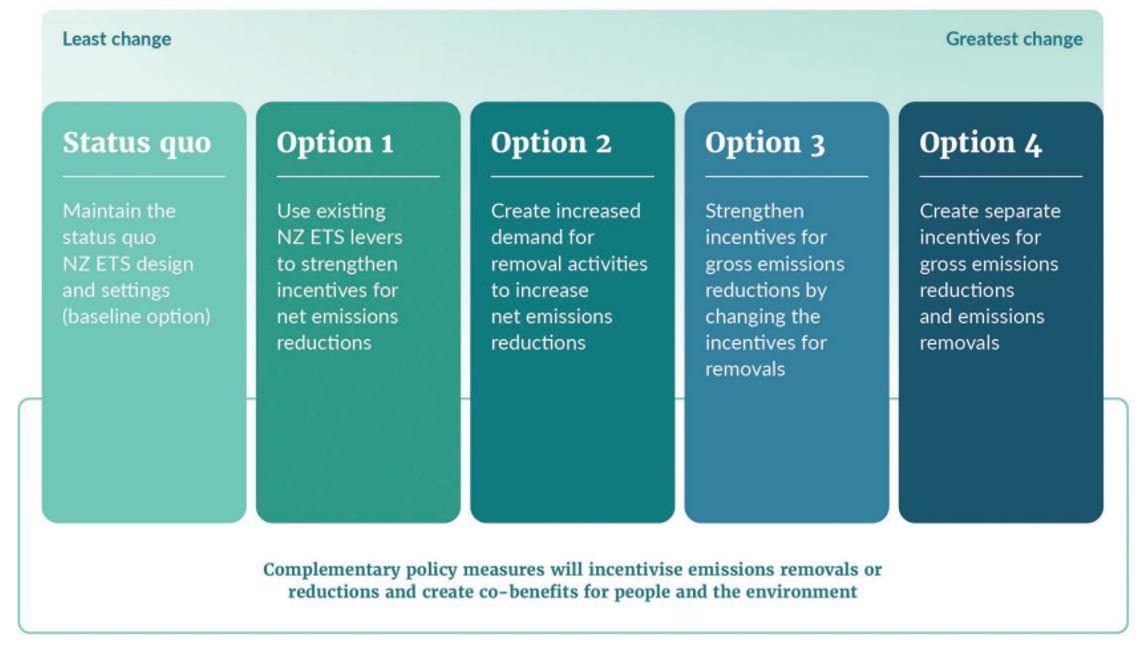

The ETS review process has commenced and to date 4 options have been proposed, as below:

Source: ETS review discussion document

These have been widely discussed in the media so we won’t go into them in detail but highlight that option 1 does not seem to add much to the current process, noting that levers already exist thru the CCC annual reviews to adjust settings.

Option 2 seems a non-starter as its not obvious why overseas buyers would want NZUs and if they could somehow use them overseas this just raises the risk NZ then needs to eventually buy units from overseas to mitigate this leakage.

This leaves options 3 and 4 as the only options that may influence a potential forestry glut. Option 3 in essence creates a price for NZUs from forestry that is linked to NZUs issued by the government, whereas option 4 more de-links these and moves forestry NZUs to a distinct market. These may not be mutually exclusive, and we could well see some form of transition from option 3 to option 4 over time as the latter is more complex and hence would take more time to implement.

Through this period, we have also seen both the March and June auctions fail to clear. Whilst these have been reported as “failed” auctions they are working as per the regulations intended. That is if sufficient bids are not received above the confidential reserve price, then the market will not clear. What this does mean though is that the unsold units roll onto the next auction if it is in the same calendar year, which means the probability of the September and December auctions clearing is low. If they both don’t clear the units get wiped and the market resets going into 2024 (which has the effect of removing some potential supply).

In July we saw the Lawyers for Climate Action NZ win a high court judgement that noted the decision by cabinet in Dec 2022 to reject the CCC advice that we talked about above was flawed, as it failed to account for NZ longer term goals and NDC. The Minister for Climate Change acknowledged this and agreed to revisit decision by Sept 2023. Then just as we were expecting very little to happen before the end of September, the government announced just a few days ago that they had reversed course and accepted last years CCC advice (which it had previously rejected) and accepted the reiterated advice from this year. Finally, we seem to have positive step to return a degree of support to NZU prices.

What does this all mean for holders of NZUs? Uncertainty is undoubtedly high, and we have seen forestry owners lobbying for everything to be left alone. This appears somewhat short sighted as forestry is a long life asset and while the current price undoubtably influences planting decisions, it is the longer term price that will ultimately determine profitability, and the risk that a tsunami of planting causes lower prices in 2030s must surely concern forestry owners. Acknowledgement should be given to MBIE for trying to fix a problem before it arrives. If the review is successful, a change could help all parties - investors into NZUs, forest owners, the government thru auction revenues and NZ as a whole by incentivising gross reductions. What is certain is that the current depressed price will not sufficiently incentivise NZ to meet the NDC and the Paris agreement.

Share article:

Other Insights

Stay updated with Castle Point Funds.

Investments

Resources

Company

Castle Point Funds

Perpetual Guardian Tower

Level 23, 191 Queen Street

Auckland 1010

PO Box 105889

Auckland 1143, New Zealand

E info@castlepointfunds.com

PG Funds Limited is the issuer and manager of the Castle Point Funds Scheme.

2025 Castle Point Funds, Inc. All rights reserved.

Privacy Policy