November 2023 - Listed property has been doing it tough

by Stephen Bennie 2023-11-16

Listed property investors may be feeling some affinity with the experience of the three little pigs.

It does feel like a big bad wolf has been huffing and puffing looking to blow their houses down for most of the past two years. The problem has been cyclical and structural headwinds blowing in tandem which has been very tough on any houses built out of bricks. Never mind any built out of straw or sticks.

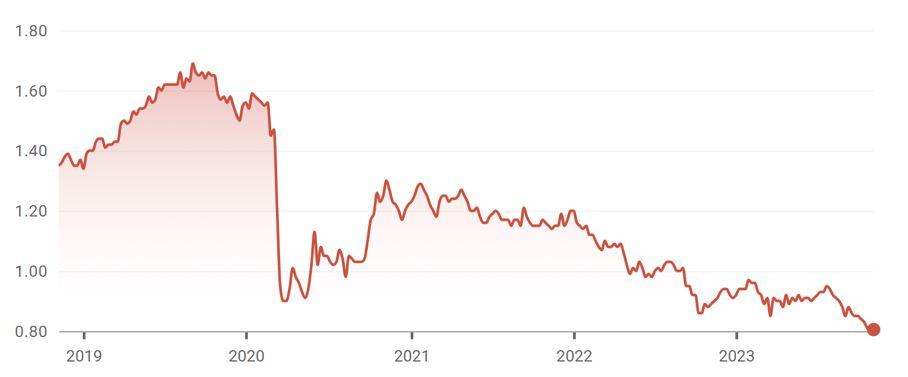

A good example of the impact of those headwinds is one of our largest and oldest listed property vehicles, Kiwi Property Group, which is currently trading over 50% lower than where it traded in 2020.

Meanwhile, Goodman Property Trust is one of New Zealand’s best-performing of the listed property vehicles, down a mere 25% from levels it traded at last year. The big bad wolf has been blowing share prices south in the listed property sector.

The Big Bad Wolf’s effect on Kiwi Property Group Source: NZX

Listed property has always been a popular place for New Zealanders to invest. It’s no secret that Kiwis love property investing, and this bias makes the listed property sector popular with retail investors, as well as many wholesale investors.

The bricks-and-mortar nature of these businesses make them straightforward to understand (and hopefully manage); they own buildings and collect rent on them. Another attraction of the sector is its focus on paying dividends, which again attracts the interest of many types of investors.

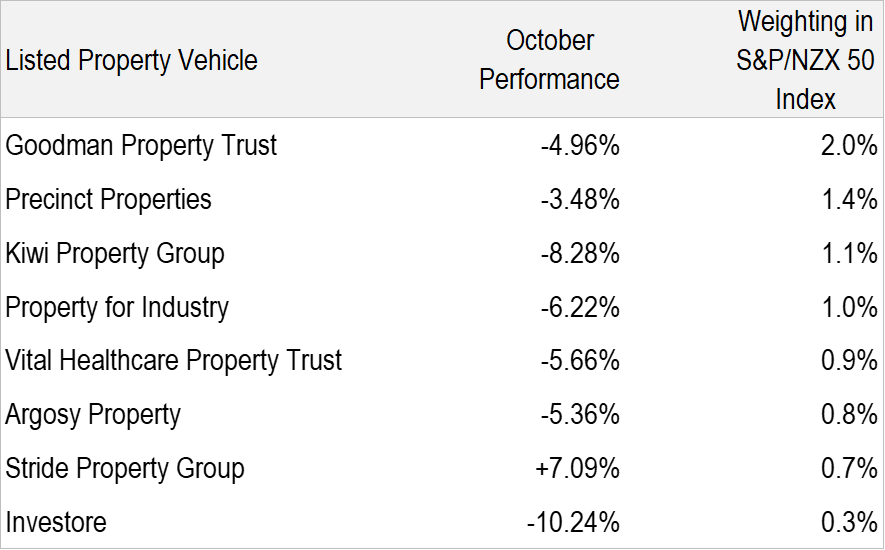

Another dynamic that investors appreciate about listed property is that the transparent business model and steady dividends should mean less volatile share price performance. This popularity is well demonstrated by the fact that 8 members of the S&P/NZX 50 are listed property vehicles, from largest to smallest; Goodman Property Trust, Precinct Properties, Kiwi Property Group, Property for Industry, Vital Healthcare Property Trust, Argosy Property, Stride Property Group and Investore.

Let’s get back to that puffing big bad wolf. Listed property will always be affected by the economic cycle, with a degree of amplification due to the habitual use of debt in the sector and the impact of interest rates on the value of its property portfolio. Economic expansion should boost tenant demand which is good for rental income. If you have that backdrop and the Reserve Bank of New Zealand, is playing Little Red Riding Hood and setting near zero interest rates, a listed property vehicle will have rising valuations on the buildings it owns as its rental income will be worth more due to the prevailing low interest rates.

That paradise has been shattered by rising interest rates and an economic slowdown which have both come in mean doses these past two years. However, these moves while sharp are not extraordinary, listed property will always experience an element of in favour and out of favour depending on the economic cycle and associated interest rate fluctuations, but something more is generally required to cause the likes of Kiwi Property Group’s share price to more than half.

That something extra, to cause even greater distress for the listed property sector, is structural change. All listed property own assets made of steel, concrete, glass and bricks (fortunately no straw or sticks) but not all are built for the same purpose. Generally, there are three main types of buildings owned;

- Office,

- Retail and

- Industrial.

Two of the three are in the process of being disrupted. Owning a shopping mall has become less attractive due to the shift to online shopping. Forecasting the impact of future interest rate moves is hard enough but forecasting the eventual impact of a structural shift is magnitudes harder. This in turn makes gauging an appropriate share price move near impossible, especially when investors were likely attracted to listed property in the first place because of its simple business model and relative stability. In such a situation, where investors are surprised and disappointed, downward share price moves can be even more precipitous.

The other disrupted type of building is, of course, Office. There had been a slow burn trend of working more from home, as businesses moved to online collaborative working tools such as Microsoft Teams and Zoom combined with the shift to "hotdesking". That trend became a runaway train due to virus lockdowns. Again, with this disruption, we don’t yet know the full impact. A combination of tenants having five-year plus rental agreements and a new status quo yet to emerge as to the new normal in terms of working from home, means we are still some time from knowing the full answer. But it’s almost certain that there will be a lower level of long-term demand for office space. Just look across to New York City where there is an estimate that 74,582,671 square feet of office space currently lies vacant[1]. For those of you that don’t do imperial measurements that is the equivalent of 26 Empire State Buildings worth of empty office space in New York City alone.

The third most common type of property got a free pass on disruption. Industrial properties are not currently subject to a significant structural challenge, so the likes of Goodman Property Trust are mainly facing the headwinds of rising interest rates and easing demand. Albeit in October another headwind emerged that affected Industrial property owners as well as the other listed property vehicles. The incoming coalition government appears highly likely to abandon a tax break that commercial property owners enjoyed. If the tax break does go, depreciation on building values will no longer be eligible for use as a tax deduction. The impact varies between the various listed property vehicles but according to research by Craigs Investment Partners the overall hit to property sector cash earnings is 5%. So, no surprise that October was another tough month.

October saw more bad news hit property investors Source: NZX

So, at what point do we know that the big bad wolf isn’t going to huff and puff and blow the house down, and that listed property will once again return to favour. It could be close to a turning point, plenty of bad news appears to now be factored into share prices. The trouble with making that call is the unknown ultimate impact of structural change on Office and Retail assets. The other slight concern is the level of debt the sector carries, if interest rates end up higher for longer, it will be another headwind on earnings.

Share article:

Other Insights

Stay updated with Castle Point Funds.

Investments

Resources

Company

Castle Point Funds

Perpetual Guardian Tower

Level 23, 191 Queen Street

Auckland 1010

PO Box 105889

Auckland 1143, New Zealand

E info@castlepointfunds.com

PG Funds Limited is the issuer and manager of the Castle Point Funds Scheme.

2025 Castle Point Funds, Inc. All rights reserved.

Privacy Policy