March 2023 - Ryman shareholders pay a hefty penalty

by Stephen Bennie 2023-03-14

Where the money went from Ryman’s recent capital raise has raised a few eyebrows.

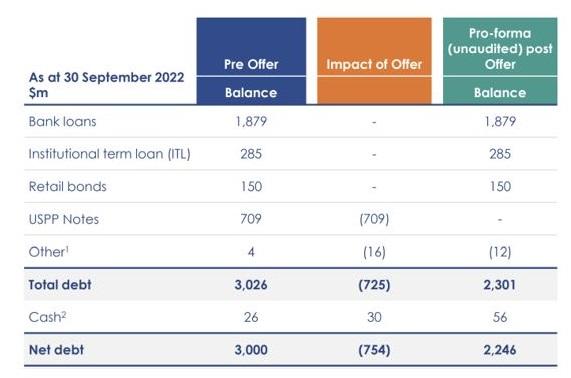

The entitlement offer that they announced on 15 February raised $902 million, and it’s not the extra $2m that caused the raised eyebrows. Nor was it the $30 million that went to the investment bankers that pulled the deal together and organised the underwriting, that cost is ballpark for this type of deal. That left Ryman with $870 million with which to reduce outstanding debt. The matter that raised eyebrows is nicely summed up by this extract from their capital raise presentation.

Extract from the Ryman capital raise presentation

Source: Ryman Healthcare

The above extract is a good illustration of the mismatch between the $870 million net amount raised and the $754 million reduction in Net Debt. The bulk of the discrepancy is the $134 million penalty incurred for the early repayment of the US Private Placement Notes (USPP Notes). $134 million isn’t small change in anyone’s book. Especially when you consider that the USPP Notes were issued in February 2021 and April 2022 only to be paid back in full in March 2023, with the extra $134 million of course.

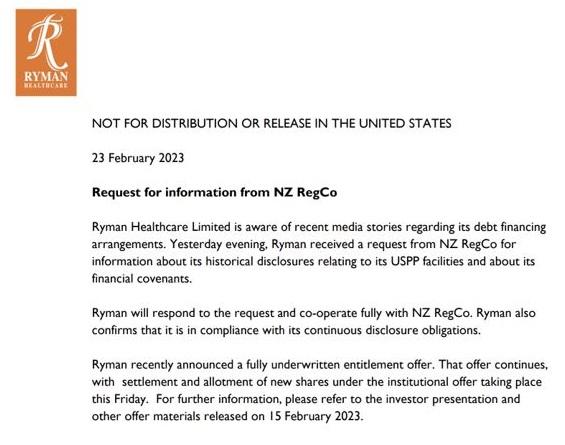

So, why did they stump up $134 million in penalty payments to the USPP Noteholders? The strong implication was that they were convinced they were going to breach its covenants and frankly there is no other credible reason for paying that substantial penalty. It’s also likely that this move was encouraged by Ryman’s local lenders that did not want the USPP Noteholders effectively becoming the senior debt holders upon the occurrence of a breach. None of this was disclosed to shareholders. Hence this announcement on 23rd February.

Announcement of NZX investigation

Source: Ryman Healthcare

This announcement has an element of irony as it’s not for distribution in the United States, the home of the USPP Noteholders who just received a stellar return from their short-term loan to Ryman.

Another interesting feature of this capital raise has been the deteriorating investor response to the deal. The structure of the raise was that institutional investors were the first to take up their rights of the new shares at $5 a share. This compares to the previous closing price of $6.40, which when diluted by the discounted capital raise equates to a theoretical ex-rights price of $6.03. Most institutional investors decided not to be diluted at $5 so took up their rights to buy shares at that level.

However, a small number of institutional investors did not take up their rights and that shortfall was offered back to institutional investors that wanted more Ryman shares. The price of these shares was determined by a competitive book build which ended up at $6 a share.

When Ryman resumed trading on 20 February it dropped to $5.75, below that book build price. Meanwhile the second phase of the capital raise, the retail offer, was underway. Just like the institutional investors, retail investors had rights to buy Ryman shares at $5, however they had a longer timeframe, that process gave them until 6th March to take up their rights. Again, most retail investors decided not to be diluted at $5 a share so took up their rights. But there was a shortfall which again was offered to institutional investors in a competitive book build. Scarcely two weeks on from clearing the shortfall at $6, institutional sentiment had clearly soured. On this occasion the clearing price in the book build was a much lower $5.25. It does tend to suggest that on reflection institutional investors have decided that this capital raise and subsequent USPP penalty payment has raised some concerns. It certainly has for the NZX.

Link to Ryman NZX announcements NZX, New Zealand’s Exchange

Share article:

Other Insights

Stay updated with Castle Point Funds.

Investments

Resources

Company

Castle Point Funds

Perpetual Guardian Tower

Level 23, 191 Queen Street

Auckland 1010

PO Box 105889

Auckland 1143, New Zealand

E info@castlepointfunds.com

PG Funds Limited is the issuer and manager of the Castle Point Funds Scheme.

2025 Castle Point Funds, Inc. All rights reserved.

Privacy Policy